Entering new markets is a crucial step for businesses looking to expand their reach, diversify their revenue streams, and mitigate risks associated with over-reliance on existing markets. However, this process is fraught with challenges that require careful planning, strategic insight, and an understanding of both local and international dynamics. In this article, we will explore effective strategies for successfully entering new markets, offering insights that can help businesses navigate this complex terrain.

Understanding Market Research and Analysis

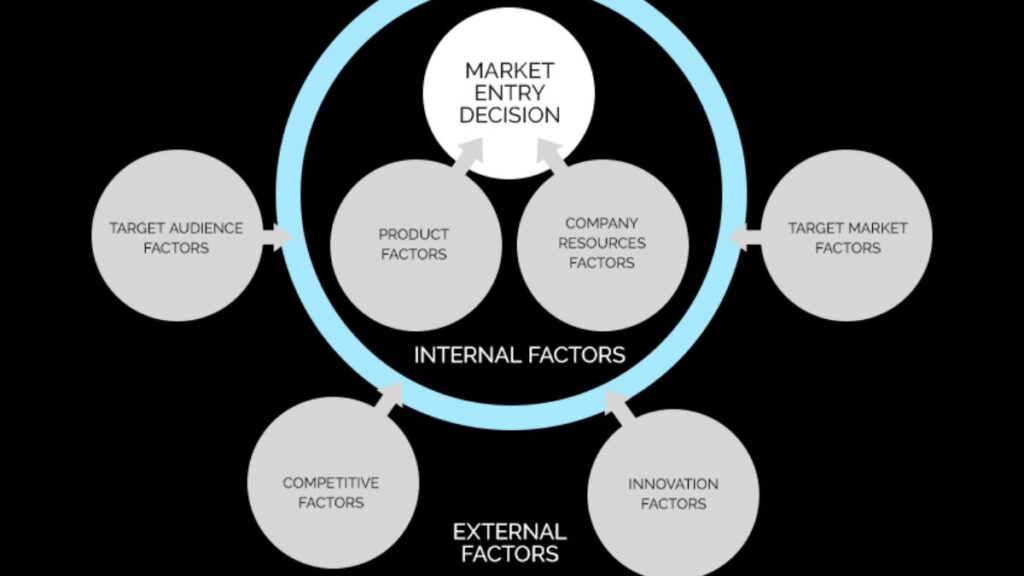

Before diving into a new market, thorough market research and analysis are essential. This phase involves gathering data about the new market’s demographics, economic conditions, consumer behavior, and competitive landscape. Market research helps businesses identify potential opportunities and threats, enabling them to tailor their strategies accordingly.

1. Identifying Market Opportunities

Begin by assessing the potential demand for your products or services in the new market. Look for gaps in the market where your offering could provide value or solve existing problems. Conduct surveys, focus groups, and interviews with local consumers to understand their needs, preferences, and purchasing behaviors. Additionally, analyze industry reports and market trends to gauge the overall health and growth potential of the market.

2. Evaluating Competitive Landscape

Understanding your competition is crucial for positioning your brand effectively. Identify key competitors in the new market, analyze their strengths and weaknesses, and evaluate their market share. This analysis will help you determine how to differentiate your offerings and what unique value propositions you can bring to the table.

Crafting a Market Entry Strategy

Once you have a clear understanding of the market, the next step is to develop a comprehensive market entry strategy. This strategy should outline how you plan to introduce your products or services, establish a presence, and achieve your business objectives.

1. Choosing the Right Entry Mode

There are several entry modes to consider, each with its advantages and challenges:

- Direct Exporting: Selling products directly to customers in the new market. This approach offers greater control but requires significant investment in distribution and logistics.

- Partnerships and Alliances: Collaborating with local businesses can provide valuable market insights and access to established distribution networks. This approach can be beneficial for leveraging local expertise and reducing entry risks.

- Franchising and Licensing: Allowing local entities to use your brand and business model in exchange for fees or royalties. This franchise my business method provides a way to expand rapidly with lower capital investment but requires stringent control over brand standards.

- Joint Ventures: Forming a new company with a local partner. This option combines resources and knowledge but involves sharing profits and control.

- Acquisitions: Buying an existing business in the target market. This strategy offers immediate market entry and established operations but involves higher costs and integration challenges.

2. Developing a Market-Specific Marketing Plan

A successful market entry also hinges on a well-crafted marketing plan tailored to the local audience. This plan should address the following elements:

- Brand Positioning: Define how you want your brand to be perceived in the new market. Consider local preferences and cultural nuances to ensure your messaging resonates with the target audience.

- Promotional Strategies: Choose appropriate promotional channels based on local media consumption habits. This might include digital marketing, traditional advertising, or public relations efforts.

- Pricing Strategy: Set pricing that reflects the local market conditions while ensuring profitability. Consider factors such as purchasing power, competitive pricing, and local cost structures.

Navigating Legal and Regulatory Requirements

Entering a new market often involves navigating a complex web of legal and regulatory requirements. Compliance with local laws is crucial for avoiding legal issues and building trust with local stakeholders.

1. Understanding Local Regulations

Research and understand the legal requirements for operating in the new market. This includes business registration, tax obligations, labor laws, and industry-specific regulations. Consult with local legal experts to ensure compliance and avoid potential pitfalls.

2. Protecting Intellectual Property

Safeguard your intellectual property (IP) by registering trademarks, patents, and copyrights in the new market. This step is essential for protecting your brand and innovations from potential infringement.

Building Relationships and Networking

Successful market entry often hinges on building strong relationships and networks within the new market. Establishing connections with local stakeholders can provide valuable insights, resources, and support.

1. Engaging with Local Partners

Form strategic alliances with local businesses, industry associations, and government agencies. These partnerships can facilitate market entry, provide access to local networks, and enhance your credibility.

2. Participating in Industry Events

Attend trade shows, conferences, and other industry events to connect with potential customers, partners, and industry experts. These events offer opportunities to showcase your products, gather market intelligence, and build relationships.

Adapting to Cultural Differences

Cultural differences can significantly impact market entry success. Understanding and respecting local customs, traditions, and business practices is essential for building rapport and avoiding misunderstandings.

1. Localizing Your Offerings

Adapt your products or services to meet local preferences and cultural norms. This might involve modifying product features, packaging, or marketing messages to align with local tastes and expectations.

2. Training and Developing Local Talent

Invest in training and developing local talent to ensure your team understands the market and can effectively address local customer needs. This approach also helps in building a positive company culture and fostering employee engagement.

Monitoring and Evaluating Performance

Once you’ve entered the new market, continuous monitoring and evaluation are critical for assessing performance and making necessary adjustments.

1. Tracking Key Performance Indicators (KPIs)

Establish KPIs to measure the success of your market entry efforts. Monitor metrics such as sales growth, market share, customer satisfaction, and profitability to gauge performance and identify areas for improvement.

2. Adjusting Strategies as Needed

Be prepared to adapt your strategies based on market feedback and performance data. Flexibility is key to addressing challenges and seizing new opportunities as they arise.

Conclusion

Entering new markets successfully requires a strategic approach that combines thorough research, careful planning, and adaptability. By understanding the market, crafting a tailored entry strategy, navigating legal requirements, building relationships, and respecting cultural differences, businesses can increase their chances of success and achieve long-term growth. Continuous monitoring and evaluation will help refine strategies and ensure that your market entry efforts remain on track. With the right approach, expanding into new markets can unlock significant opportunities and drive your business forward.